Southern Africa Special Report: Uncertain economic recovery prospects due to COVID-19 likely to negatively impact political stability, security across the region

This report was written by: Shaantanu Shankar, Senior Analyst for Southern Africa

And edited by: Aarushi Tibrewala, Senior Intelligence Manager for Sub-Saharan Africa

Executive Summary

- Southern Africa experienced the most pronounced COVID-19 pandemic-induced economic impact on the continent, reporting an economic contraction of seven percent in 2020. With economic recovery linked to a roll-back of COVID-19 restrictions, among other factors, delayed vaccine deployment poses a significant challenge to economic recovery.

- The pandemic has further exacerbated the situation across countries already in the midst of, or on the verge of, economic crisis. Regional economic dependencies on mineral resources, tourism, and unimpeded cross-border trade to a large extent have accentuated pandemic-induced impacts.

- On the ground, the persisting economic crisis is likely to manifest into sporadic supply disruptions and increased cost of basic supplies including food and fuel, overall increasing vulnerability of low income populations, who constitute the majority socioeconomic demographic across the region.

- At the government level, the situation is likely to manifest into increasing budgetary constraints exacerbating existing public debt challenges. In this regard, increased labor actions in critical sectors such as healthcare, transport, power, mining and administration could lead to disruptions to government services and critical utility provisions such as power.

- The overall increase in socioeconomic stress could manifest into an overall increase in civil unrest, especially in the form of anti-government protests and demonstrations as seen in Angola and South Africa. It could also potentially trigger increasing anti-incumbency sentiment and impact political stability through weakening the respective ruling parties’ authority across the region.

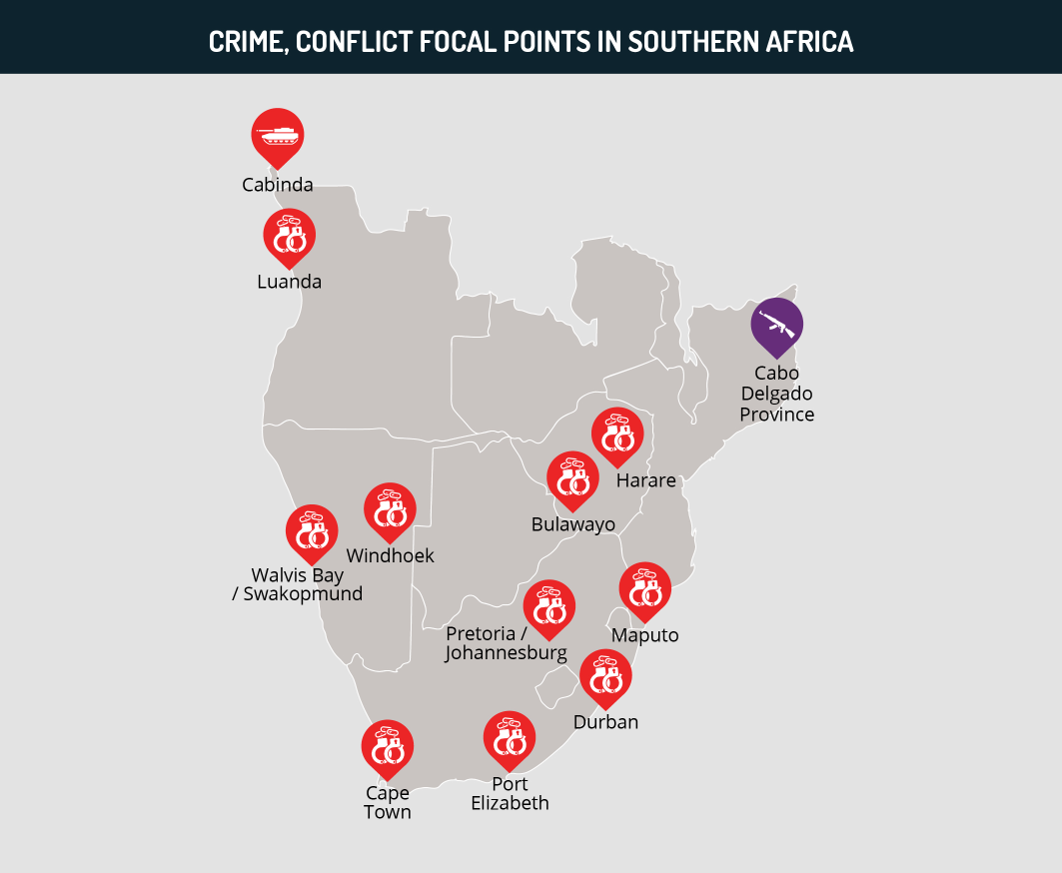

- Heightened socioeconomic stress and associated increases in unemployment and poverty carry the potential to lead to an increase in criminal activity. In this context, regional urban localities such as Luanda, Johannesburg, Cape Town, Durban, Harare, Maputo, and Windhoek are particularly vulnerable. Additionally, given the possibility of medicine and vaccine shortages, the region could see a rise in counterfeit medicine trade over the coming months.

Current Situation

- According to the African Development Bank (AfDB) African Economic Outlook published on March 12, the African continent moved into a recession in 2020 for the first time in 25 years, reporting that 30 million Africans were pushed into extreme poverty in 2020 due to the COVID-19 pandemic.

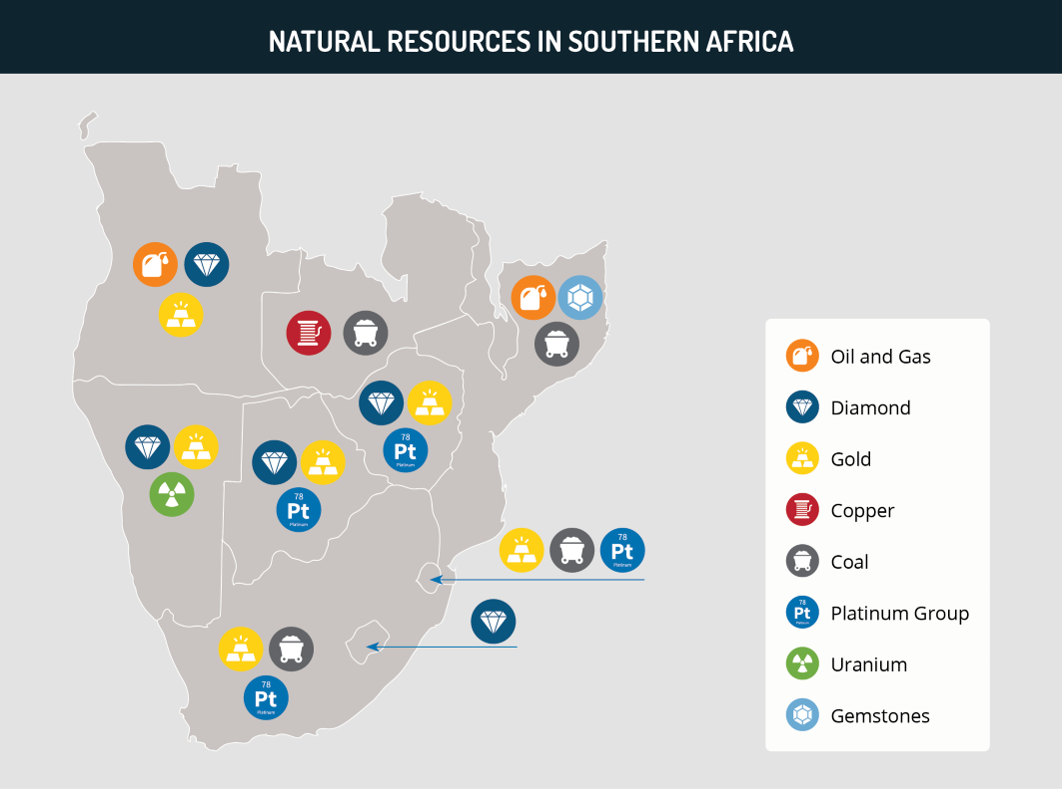

- Southern Africa experienced the most pronounced pandemic-induced economic impact, recording an economic contraction of seven percent in 2020. The document also detailed that the pandemic’s economic impact was most acute in oil and gas, mineral, and tourism driven economies across the continent.

Assessments & Forecast

COVID-19 crisis in India to further delay vaccine deployment across Africa, likely to impact post-pandemic economic recovery

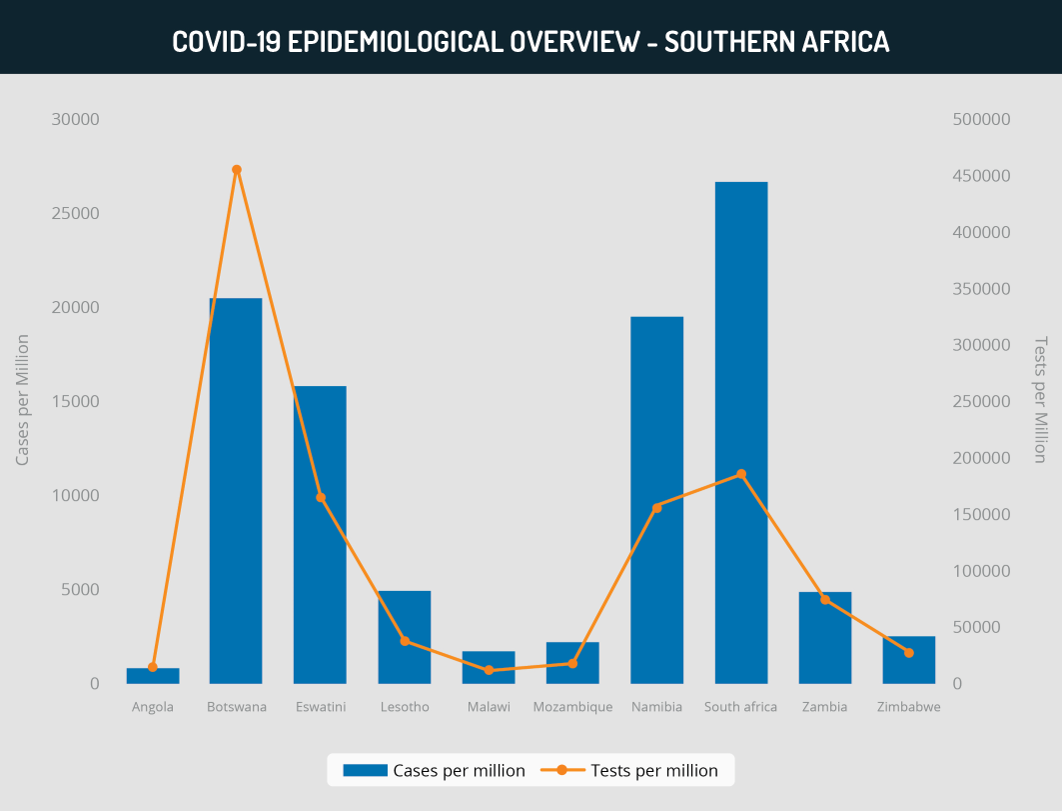

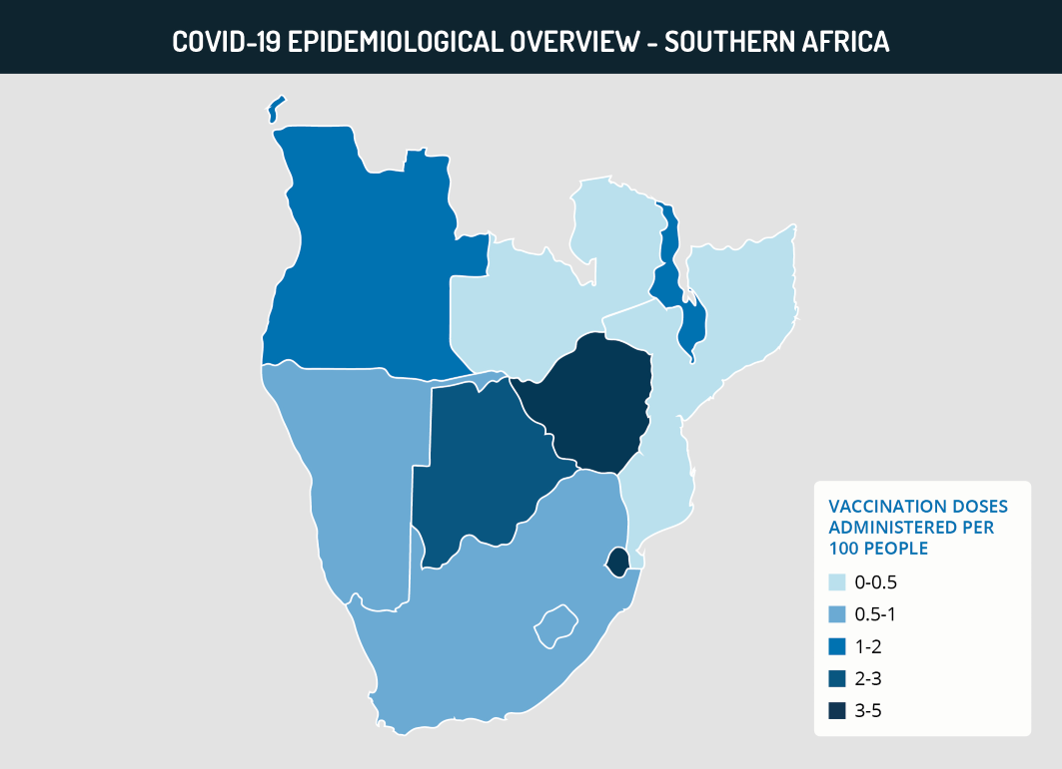

- A little over a year since the detection of the first COVID-19 case in Africa, several African countries have initiated national vaccination programs. However, issues related to supply shortages, delayed deliveries, logistical challenges, and financial access have led to shortfalls across the continent. Furthermore, despite entering into deals with various suppliers from both the West as well as Russia, China, and India, vaccine supplies remain limited as suppliers continue to face challenges in balancing domestic demand with vaccine exports. Currently, given the situation, the continent is dependent on the World Health Organization (WHO) sponsored COVAX alliance whose deliveries have kick started vaccination programs in several countries. However, COVAX supplies until May 2021 cover on average approximately five percent of total requirements.

- Moreover, India represents Africa’s leading trade partner in the pharmaceutical sector accounting for close to 20 percent of Africa’s total medicinal imports. India is also the major global production hub for the AstraZeneca vaccine, which is critical for the COVAX alliance vaccine deliveries to the continent. India is currently experiencing a devastating second wave that has led to a severe health crisis and an associated acute shortage of medical supplies and vaccines. FORECAST: Given Africa’s dependence on India for vaccines and other medicinal supplies, it is possible that the crisis in India will lead to disruptions in medicinal exports to Africa. This will likely lead to the Indian government compelling Indian private pharmaceutical manufacturers to route vaccines and other medicine supplies for consumption inside India. These disruptions could further undermine the health response of African countries already challenged by supply shortages and limited pharmaceutical manufacturing capabilities.

- FORECAST: Given the situation, Africa is expected to have a much longer timeline to achieve herd immunity in the majority of countries. This is likely to extend the socioeconomic, political, and civil impact of the COVID-19 pandemic as well, as countries are also unlikely to be able to fully resume economic activity until a comprehensive degree of immunization has been achieved. In this context, economic forecasts for recovery in 2021 are considerably uncertain due to a combination of external and domestic risk factors, including sudden surges and increases related to a potential third wave, which is expected to hit South Africa over the coming weeks.

Extended impact of the pandemic, associated uncertainties likely to extend regional macroeconomic crisis

- Pandemic-induced factors have also impeded recovery prospects and negatively contributed to the situation in Southern African countries that were already in the midst of or on the verge of economic crisis. In this context, the pandemic likely hastened economic deterioration in Zambia and Zimbabwe, with Zambia becoming the only African country to default on sovereign bond debt in November 2020, and Zimbabwe experiencing a severe inflationary crisis from April to September 2020. Meanwhile, the fall in oil prices and demand through 2020 contributed to a fourth consecutive recession in Angola, and the first recession in 25 years in Mozambique.

- These factors also accelerated downward trends across the region leading to major credit ratings similarly revising downward country credit ratings and other outlooks. Several countries are dependent on accessing finance from international markets, with negative evaluations effectively increasing the cost of loans and other financial instruments. This is significant given that poor economic performance and associated negative credit outlooks could prevent countries from accessing critical financial relief grants and similar instruments from institutions such as the International Monetary Fund (IMF) and other international partners.

- FORECAST: These constraints could adversely impact financial stability given that they could encourage inflation and other recessionary trends. Furthermore, at the micro level, national budgets are similarly dependent on external financial assistance and disruptions to these flows could spill over into budgetary constraints as well. This is likely to further inhibit economic recovery prospects, potentially extending the macroeconomic crisis across the region.

Extended barriers to cross-border trade likely to trigger critical supply disruptions, exacerbate socioeconomic vulnerabilities of local populations in Southern Africa

- The Southern Africa region is economically and socially well-connected due to common market linkages through various regional organizations. South Africa, a major supplier of basic commodities across the region, continues to experience logistical challenges at major border posts, which are likely to increase subject to the pandemic-induced restrictions. With six land-locked countries, populations and domestic markets are highly dependent on the unhindered flow of cross-border trade. Persisting restrictions on the transportation sector due to border restrictions and adoption of new standard operating procedures have already resulted in longer transit times and higher transport costs. FORECAST: Given that these linkages are critical for the region’s economic growth, delayed immunization is likely to translate to continued disruptions and logistical delays at land borders due to tightened border protocols and border movement restrictions.

- In this context, the pandemic has had a strong impact on food insecurity across the continent, a situation that has been exacerbated by border closures, lockdowns, and associated supply disruptions. Reports already indicate sharp increases in populations facing acute food insecurity in Angola, Malawi, Namibia, Zambia, Zimbabwe, and Mozambique through 2020 and 2021. FORECAST: Barriers to cross-border transport are likely to persist, which could lead to persisting food price increases over the coming months. This is likely to continue to represent a challenge to government response measures, with the situation likely to encourage increasing food costs, and in turn further impacting food security among vulnerable populations. Additionally, populations are particularly vulnerable to sudden surges in COVID-19 cases, which would force authorities to intensify border restrictions and lead to periods of uncertainty related to basic good supplies. This, in turn, could also manifest into increased price volatility of critical supplies such as fuel.

Dependence on mineral resources, tourism sectors likely to undermine economic recovery prospects across the region

- Southern Africa is characterized by mostly resource-intensive economies, which have especially been heavily impacted by disruptions to commodity prices and demand through the pandemic. Additionally, despite a larger degree of diversification in the region’s largest economy, South Africa, the mining industry plays a very important role both in terms of revenue as well as employment generation. In this regard, economic recovery in the region is likely to remain partially dependent on two critical market factors, a sustained rebound in commodity prices and economic recovery in major export markets.

- In addition to resource-based industry, tourism is also another critical economic sector across the whole region, with countries hinging recovery prospects to the resumption of tourism and related activities through the year. This is further complicated by the fact that recovery is also linked to economic and health trends both in Africa as well as other locations around the world. Furthermore, the informal sectors of the economy, which provide livelihood opportunities to a majority of local communities, have already been severely impacted due to the consequences of lockdowns and associated government health regulations.

- FORECAST: Both these sectors are critically dependent on a rollback of pandemic-induced restrictions, which is likely to be deferred by delays to national immunization plans in addition to its dependency on other external risk factors. Low-income communities form a large proportion of the region’s population and are most vulnerable socioeconomically. To this point, extended periods of lockdowns and related restrictions are likely to further exacerbate socioeconomic stress, and in turn, increase income inequality as well which could manifest into heightened social disgruntlement and political animosity.

Increasing national budgetary constraints, disruptions to government services, utility provisions likely to increase anti-government sentiment

- At the government level, the economic situation is likely to translate into pressure on public finances and budgetary constraints. Public sector debt is already a serious challenge to economic growth, especially in South Africa and Zimbabwe, where the governments are consistently challenged by union strikes over payment grievances and salary demands. Furthermore, union strikes have been reported across the region in critical sectors such as healthcare, transport, power, mining, and administration, leading to temporary service disruptions. The inability to appease the relatively large number of public sector workers has the potential to weaken the ruling parties’ political authority as well.

- Civil society forces in South Africa have vocalized their opposition towards the government’s plans for the reform of ailing state-owned industries, highlighting the existing opposition to privatization and public sector retrenchments. FORECAST: In this context, the South African government’s inability to meet union demands in a timely manner could further encourage labor strikes and associated disruptions to government services. This could also lead to delays in implementing public sector reform plans, which are important to stimulate economic recovery. This could also manifest into continued disruptions to business continuity due to potential public service disruptions.

Economic uncertainty to further delay critical power sector developments, exacerbate electricity shortages

- Several countries in the region currently face considerable power deficits, with load-shedding a fairly common feature in South Africa, Zambia, and Zimbabwe. Furthermore, power sector developments are by and large dependent on international financing and global supply chain linkages, with supply and logistical disruptions during the initial phases of the pandemic in 2020 leading to delays to several critical regional power sector projects, including the Kafue Gorge Hydropower Project in Zambia. Delays to critical power sector developments also hold the potential to derail power sector reform plans. Such a situation could also exacerbate existing debt crises across these countries’ respective public power sector players Eskom (South Africa), Zesco (Zambia), and Zimbabwe Electricity Supply Authority (Zesa), and make power sector recovery in these countries increasingly challenging. FORECAST: In all these countries, an extended power crisis could potentially undermine recovery prospects especially given reports of mining operations also being disrupted due to the shortfalls.

- The potential impact on the government’s ability to steadily provide utilities, particularly electricity, could also impede political authority. In this context, the ongoing economic crisis in Zambia is likely to seriously undermine the government’s plans to increase power supply at a crucial pre-electoral phase. FORECAST: Limited power supply, which is likely to impact industrial output, could also lead to increased political disenchantment with the ruling Patriotic Front (PF), as the country faces other pressing economic concerns due to mounting debt. Furthermore, the situation is exacerbated by increasing fuel and food prices. In this context, the opposition is liable to capitalize on presenting the government’s alleged economic mismanagement as exacerbating socioeconomic stress among local communities. With general elections slated to be held in August, political tensions are poised to remain extremely high leading into the pre-electoral phase.

Persisting economic crisis to impact political stability across Southern Africa

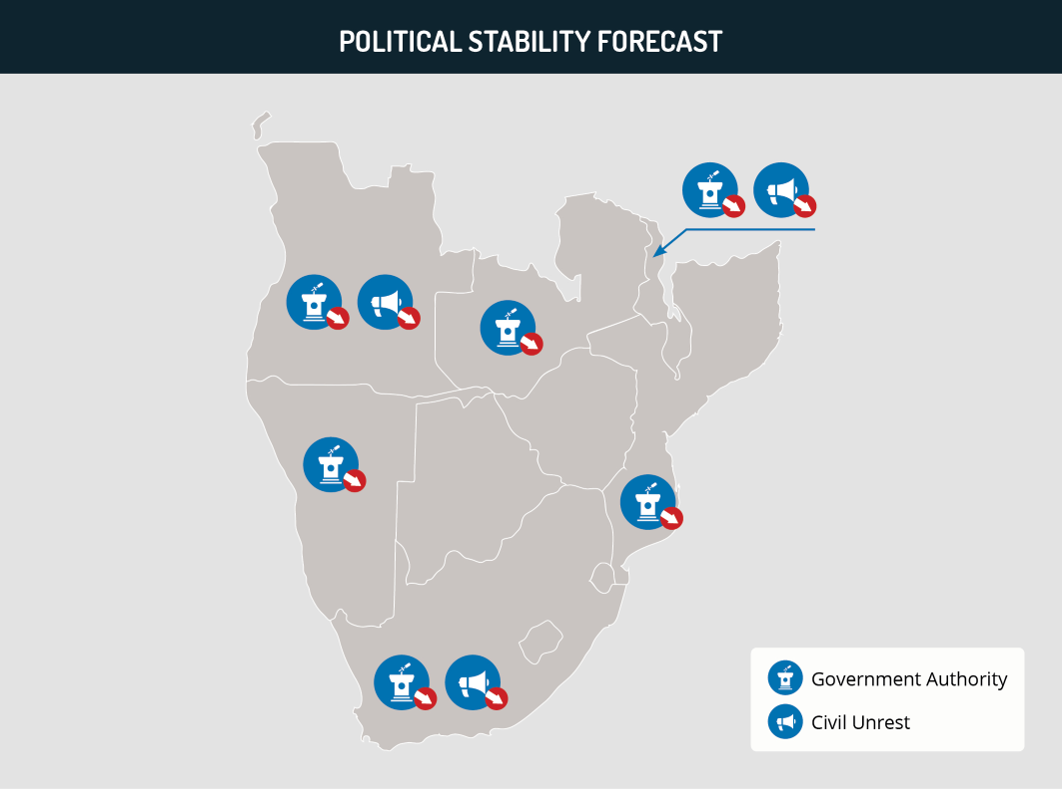

- Given the uncertainty associated with economic recovery prospects, there is an increased likelihood of the overall increased socioeconomic stress and associated public grievances translating into an increase in civil unrest, especially in the form of anti-government protests and demonstrations. This has already been seen in Angola and South Africa, where public grievances against pandemic restrictions and forceful enforcement of these restrictions by authorities led to a series of anti-government protests through 2020.

- In Angola, the persisting economic crisis triggered a series of demonstrations against the People’s Movement for the Liberation of Angola (MPLA), the ruling party for 45 years in Angola, in response to perceived government economic mismanagement over the years. In 2020, there was a notable uptick in protest activity through the year, with the pandemic further heightening economic stress and increasing social vulnerability, a major factor driving anti-government sentiment. The major opposition parties have also supported civil society protests in attempts to politically capitalize on the anti-incumbency sentiment prevailing and increasingly manifesting into civil action. FORECAST: Persisting economic deterioration could potentially impact the MPLA’s political consolidation going into municipal elections, which were postponed to 2022.

- In South Africa, similar economic concerns along with a corruption scandal around COVID-19 financial resources also triggered nationwide anti-government protests against the ruling African National Congress (ANC). Major labor union organizations such as Congress of South African Trade Unions (COSATU), which constitute a significant electoral support base for the ANC, have led protests, pressuring the government and the ANC to take action on corruption and other socioeconomic issues. The increasing political pressure to act on the issue indirectly heightened intra-party tensions and factionalism over perceptions of President Cyril Ramaphosa persecuting rival political factions led by former President Jacob Zuma and ANC Secretary General Ace Magashule. FORECAST: The heightened intra-party tensions could undermine the ANC’s political stability, especially ahead of the local elections slated for August 2021.

- FORECAST: Moreover, persisting socioeconomic grievances could potentially trigger increasing anti-incumbency sentiment and weaken the political standing of dominant political forces across the region as seen in Namibia where the South-West Africa People’s Organization (SWAPO) lost considerable ground to the opposition during the municipal elections in November 2020. Furthermore, corruption exposures in the management of COVID-19 finances is another factor that could potentially increase anti-government sentiment, as seen in both South Africa and Malawi. Additionally, an extended economic crisis could also lead to a weakening of other dominant national political forces as well.

Extended pandemic impacts likely to further entrench government authoritarianism in Zimbabwe

- Moreover, extended pandemic impacts are likely to increase concerns related to the government exploiting the health crisis to restrict anti-government activity and crackdown on the population’s rights to free speech and public demonstration. Authorities have already utilized existing emergency and disaster management legislations restrictions to intimidate journalists and activists critical of the government’s management of the pandemic in Angola, Malawi, Mozambique, Zambia, and Zimbabwe.

- In Zimbabwe, the government has utilized the pandemic to further extend its authority and repress the opposition along with any attempts at political protests. Major opposition figures and civil society leaders including journalist Hopewell Chin’ono and Movement for Democratic Change – Alliance (MDC-A) leader Job Sikhala have been arrested with the government effectively suppressing the manifestation of any political dissent. Meanwhile, the government has also resorted to increasing currency and foreign exchange regulation in the economy to counter very steep inflationary trends through 2020.

- FORECAST: Given the situation, the government is likely to continue to utilize social restrictions to repress perceived sources of political dissent and maintain its crackdown against civil society mobilizations, demonstrations, and other such anti-government public events. This could lead to sporadic disruptions to internet and telecommunication services given the government’s disposition to strictly regulate social media and other perceived anti-government media outlets around planned opposition protests.

Increasing socioeconomic stress, vulnerability of low-income populations to manifest into increasing criminal activity

- FORECAST: Most significantly, heightened socioeconomic stress and associated increases in unemployment and poverty carry the potential to lead to an increase in criminal activity. While initial lockdown restrictions witnessed a reduction in crime rates across the region, the trend has reversed over the second half of 2020 and the first quarter of 2021. This is especially a concern in South Africa, Angola, Namibia, and Zimbabwe, who are four out of the top six African countries worst affected by criminality.

- Given the concentration of low income communities in urban localities where crime is heavily entrenched across these countries, increasing criminal activity is particularly likely to affect regional urban localities. FORECAST: The inability of the government to effectively counter these increases is likely to encourage civilian vigilantism, as witnessed in Angola and South Africa. The potential for vigilante justice to spark mob violence could further deteriorate public trust in law enforcement capacity and generally lead to increased insecurity and a potential breakdown in law and order. Such sentiment is likely to further encourage civilian vigilantism, highlighting the risk of cyclical violence between security forces and citizens.

- In Cape Town, South Africa, organized criminal groups and gangs have effectively increased their authority over low income suburban communities capitalizing on the socioeconomic vulnerability of populations there. Criminal activity has also targeted service delivery vehicles, including government relief packages, further entrenching gang dominance over local communities. Similarly, other provinces majorly affected by crime including Gauteng and KwaZulu-Natal have seen an increase in crime over the second half of 2020. FORECAST: Going forward, the situation is likely to translate into an increase in criminal entrenchment across crime focal points in South Africa.

- Additionally, with the countries continuing to face issues in terms of procuring adequate vaccine and medicine supplies, illegal trade in counterfeit vaccines holds the potential to impact national and regional health security. The rush to acquire COVID-19 vaccines across the region could represent a potentially lucrative prospect for organized criminal groups to profit from counterfeit vaccine networks. This was illustrated through the dismantling of a counterfeit vaccine production network with suspected links to China in South Africa in November 2020. FORECAST: While there have been no other reported incidents related to counterfeit vaccines, the potential remains. Meanwhile, illegal trade in counterfeit medicines is likely to continue to pose concerns for national health security.

Recommendations

- Those operating or residing in Southern Africa over the coming weeks and months are advised to practice increased health precautions due to potential exposure to coronavirus and remain cognizant of authorities’ instructions regarding updated quarantines and health procedures.

- Consult with your healthcare provider before traveling. Immediately consult a doctor if you are concerned that you have potentially contracted the disease. Only procedure medication and medical advice from vetted professional institutions and remain cognizant of any fake or counterfeit medication.

- It is advised to remain cognizant of potential disruptions to business continuity over the possibility of increased civil unrest and anti-government protests over the coming months.

- Additionally, it is advised to maintain heightened vigilance over the risk of increasing criminal activity. Foreigners are advised to maintain a low profile due to the heightened crime risk.

This report was written by: Shaantanu Shankar, Senior Analyst for Southern Africa

And edited by: Aarushi Tibrewala, Senior Intelligence Manager for Sub-Saharan Africa

Executive Summary

- Southern Africa experienced the most pronounced COVID-19 pandemic-induced economic impact on the continent, reporting an economic contraction of seven percent in 2020. With economic recovery linked to a roll-back of COVID-19 restrictions, among other factors, delayed vaccine deployment poses a significant challenge to economic recovery.

- The pandemic has further exacerbated the situation across countries already in the midst of, or on the verge of, economic crisis. Regional economic dependencies on mineral resources, tourism, and unimpeded cross-border trade to a large extent have accentuated pandemic-induced impacts.

- On the ground, the persisting economic crisis is likely to manifest into sporadic supply disruptions and increased cost of basic supplies including food and fuel, overall increasing vulnerability of low income populations, who constitute the majority socioeconomic demographic across the region.

- At the government level, the situation is likely to manifest into increasing budgetary constraints exacerbating existing public debt challenges. In this regard, increased labor actions in critical sectors such as healthcare, transport, power, mining and administration could lead to disruptions to government services and critical utility provisions such as power.

- The overall increase in socioeconomic stress could manifest into an overall increase in civil unrest, especially in the form of anti-government protests and demonstrations as seen in Angola and South Africa. It could also potentially trigger increasing anti-incumbency sentiment and impact political stability through weakening the respective ruling parties’ authority across the region.

- Heightened socioeconomic stress and associated increases in unemployment and poverty carry the potential to lead to an increase in criminal activity. In this context, regional urban localities such as Luanda, Johannesburg, Cape Town, Durban, Harare, Maputo, and Windhoek are particularly vulnerable. Additionally, given the possibility of medicine and vaccine shortages, the region could see a rise in counterfeit medicine trade over the coming months.

Current Situation

- According to the African Development Bank (AfDB) African Economic Outlook published on March 12, the African continent moved into a recession in 2020 for the first time in 25 years, reporting that 30 million Africans were pushed into extreme poverty in 2020 due to the COVID-19 pandemic.

- Southern Africa experienced the most pronounced pandemic-induced economic impact, recording an economic contraction of seven percent in 2020. The document also detailed that the pandemic’s economic impact was most acute in oil and gas, mineral, and tourism driven economies across the continent.

Assessments & Forecast

COVID-19 crisis in India to further delay vaccine deployment across Africa, likely to impact post-pandemic economic recovery

- A little over a year since the detection of the first COVID-19 case in Africa, several African countries have initiated national vaccination programs. However, issues related to supply shortages, delayed deliveries, logistical challenges, and financial access have led to shortfalls across the continent. Furthermore, despite entering into deals with various suppliers from both the West as well as Russia, China, and India, vaccine supplies remain limited as suppliers continue to face challenges in balancing domestic demand with vaccine exports. Currently, given the situation, the continent is dependent on the World Health Organization (WHO) sponsored COVAX alliance whose deliveries have kick started vaccination programs in several countries. However, COVAX supplies until May 2021 cover on average approximately five percent of total requirements.

- Moreover, India represents Africa’s leading trade partner in the pharmaceutical sector accounting for close to 20 percent of Africa’s total medicinal imports. India is also the major global production hub for the AstraZeneca vaccine, which is critical for the COVAX alliance vaccine deliveries to the continent. India is currently experiencing a devastating second wave that has led to a severe health crisis and an associated acute shortage of medical supplies and vaccines. FORECAST: Given Africa’s dependence on India for vaccines and other medicinal supplies, it is possible that the crisis in India will lead to disruptions in medicinal exports to Africa. This will likely lead to the Indian government compelling Indian private pharmaceutical manufacturers to route vaccines and other medicine supplies for consumption inside India. These disruptions could further undermine the health response of African countries already challenged by supply shortages and limited pharmaceutical manufacturing capabilities.

- FORECAST: Given the situation, Africa is expected to have a much longer timeline to achieve herd immunity in the majority of countries. This is likely to extend the socioeconomic, political, and civil impact of the COVID-19 pandemic as well, as countries are also unlikely to be able to fully resume economic activity until a comprehensive degree of immunization has been achieved. In this context, economic forecasts for recovery in 2021 are considerably uncertain due to a combination of external and domestic risk factors, including sudden surges and increases related to a potential third wave, which is expected to hit South Africa over the coming weeks.

Extended impact of the pandemic, associated uncertainties likely to extend regional macroeconomic crisis

- Pandemic-induced factors have also impeded recovery prospects and negatively contributed to the situation in Southern African countries that were already in the midst of or on the verge of economic crisis. In this context, the pandemic likely hastened economic deterioration in Zambia and Zimbabwe, with Zambia becoming the only African country to default on sovereign bond debt in November 2020, and Zimbabwe experiencing a severe inflationary crisis from April to September 2020. Meanwhile, the fall in oil prices and demand through 2020 contributed to a fourth consecutive recession in Angola, and the first recession in 25 years in Mozambique.

- These factors also accelerated downward trends across the region leading to major credit ratings similarly revising downward country credit ratings and other outlooks. Several countries are dependent on accessing finance from international markets, with negative evaluations effectively increasing the cost of loans and other financial instruments. This is significant given that poor economic performance and associated negative credit outlooks could prevent countries from accessing critical financial relief grants and similar instruments from institutions such as the International Monetary Fund (IMF) and other international partners.

- FORECAST: These constraints could adversely impact financial stability given that they could encourage inflation and other recessionary trends. Furthermore, at the micro level, national budgets are similarly dependent on external financial assistance and disruptions to these flows could spill over into budgetary constraints as well. This is likely to further inhibit economic recovery prospects, potentially extending the macroeconomic crisis across the region.

Extended barriers to cross-border trade likely to trigger critical supply disruptions, exacerbate socioeconomic vulnerabilities of local populations in Southern Africa

- The Southern Africa region is economically and socially well-connected due to common market linkages through various regional organizations. South Africa, a major supplier of basic commodities across the region, continues to experience logistical challenges at major border posts, which are likely to increase subject to the pandemic-induced restrictions. With six land-locked countries, populations and domestic markets are highly dependent on the unhindered flow of cross-border trade. Persisting restrictions on the transportation sector due to border restrictions and adoption of new standard operating procedures have already resulted in longer transit times and higher transport costs. FORECAST: Given that these linkages are critical for the region’s economic growth, delayed immunization is likely to translate to continued disruptions and logistical delays at land borders due to tightened border protocols and border movement restrictions.

- In this context, the pandemic has had a strong impact on food insecurity across the continent, a situation that has been exacerbated by border closures, lockdowns, and associated supply disruptions. Reports already indicate sharp increases in populations facing acute food insecurity in Angola, Malawi, Namibia, Zambia, Zimbabwe, and Mozambique through 2020 and 2021. FORECAST: Barriers to cross-border transport are likely to persist, which could lead to persisting food price increases over the coming months. This is likely to continue to represent a challenge to government response measures, with the situation likely to encourage increasing food costs, and in turn further impacting food security among vulnerable populations. Additionally, populations are particularly vulnerable to sudden surges in COVID-19 cases, which would force authorities to intensify border restrictions and lead to periods of uncertainty related to basic good supplies. This, in turn, could also manifest into increased price volatility of critical supplies such as fuel.

Dependence on mineral resources, tourism sectors likely to undermine economic recovery prospects across the region

- Southern Africa is characterized by mostly resource-intensive economies, which have especially been heavily impacted by disruptions to commodity prices and demand through the pandemic. Additionally, despite a larger degree of diversification in the region’s largest economy, South Africa, the mining industry plays a very important role both in terms of revenue as well as employment generation. In this regard, economic recovery in the region is likely to remain partially dependent on two critical market factors, a sustained rebound in commodity prices and economic recovery in major export markets.

- In addition to resource-based industry, tourism is also another critical economic sector across the whole region, with countries hinging recovery prospects to the resumption of tourism and related activities through the year. This is further complicated by the fact that recovery is also linked to economic and health trends both in Africa as well as other locations around the world. Furthermore, the informal sectors of the economy, which provide livelihood opportunities to a majority of local communities, have already been severely impacted due to the consequences of lockdowns and associated government health regulations.

- FORECAST: Both these sectors are critically dependent on a rollback of pandemic-induced restrictions, which is likely to be deferred by delays to national immunization plans in addition to its dependency on other external risk factors. Low-income communities form a large proportion of the region’s population and are most vulnerable socioeconomically. To this point, extended periods of lockdowns and related restrictions are likely to further exacerbate socioeconomic stress, and in turn, increase income inequality as well which could manifest into heightened social disgruntlement and political animosity.

Increasing national budgetary constraints, disruptions to government services, utility provisions likely to increase anti-government sentiment

- At the government level, the economic situation is likely to translate into pressure on public finances and budgetary constraints. Public sector debt is already a serious challenge to economic growth, especially in South Africa and Zimbabwe, where the governments are consistently challenged by union strikes over payment grievances and salary demands. Furthermore, union strikes have been reported across the region in critical sectors such as healthcare, transport, power, mining, and administration, leading to temporary service disruptions. The inability to appease the relatively large number of public sector workers has the potential to weaken the ruling parties’ political authority as well.

- Civil society forces in South Africa have vocalized their opposition towards the government’s plans for the reform of ailing state-owned industries, highlighting the existing opposition to privatization and public sector retrenchments. FORECAST: In this context, the South African government’s inability to meet union demands in a timely manner could further encourage labor strikes and associated disruptions to government services. This could also lead to delays in implementing public sector reform plans, which are important to stimulate economic recovery. This could also manifest into continued disruptions to business continuity due to potential public service disruptions.

Economic uncertainty to further delay critical power sector developments, exacerbate electricity shortages

- Several countries in the region currently face considerable power deficits, with load-shedding a fairly common feature in South Africa, Zambia, and Zimbabwe. Furthermore, power sector developments are by and large dependent on international financing and global supply chain linkages, with supply and logistical disruptions during the initial phases of the pandemic in 2020 leading to delays to several critical regional power sector projects, including the Kafue Gorge Hydropower Project in Zambia. Delays to critical power sector developments also hold the potential to derail power sector reform plans. Such a situation could also exacerbate existing debt crises across these countries’ respective public power sector players Eskom (South Africa), Zesco (Zambia), and Zimbabwe Electricity Supply Authority (Zesa), and make power sector recovery in these countries increasingly challenging. FORECAST: In all these countries, an extended power crisis could potentially undermine recovery prospects especially given reports of mining operations also being disrupted due to the shortfalls.

- The potential impact on the government’s ability to steadily provide utilities, particularly electricity, could also impede political authority. In this context, the ongoing economic crisis in Zambia is likely to seriously undermine the government’s plans to increase power supply at a crucial pre-electoral phase. FORECAST: Limited power supply, which is likely to impact industrial output, could also lead to increased political disenchantment with the ruling Patriotic Front (PF), as the country faces other pressing economic concerns due to mounting debt. Furthermore, the situation is exacerbated by increasing fuel and food prices. In this context, the opposition is liable to capitalize on presenting the government’s alleged economic mismanagement as exacerbating socioeconomic stress among local communities. With general elections slated to be held in August, political tensions are poised to remain extremely high leading into the pre-electoral phase.

Persisting economic crisis to impact political stability across Southern Africa

- Given the uncertainty associated with economic recovery prospects, there is an increased likelihood of the overall increased socioeconomic stress and associated public grievances translating into an increase in civil unrest, especially in the form of anti-government protests and demonstrations. This has already been seen in Angola and South Africa, where public grievances against pandemic restrictions and forceful enforcement of these restrictions by authorities led to a series of anti-government protests through 2020.

- In Angola, the persisting economic crisis triggered a series of demonstrations against the People’s Movement for the Liberation of Angola (MPLA), the ruling party for 45 years in Angola, in response to perceived government economic mismanagement over the years. In 2020, there was a notable uptick in protest activity through the year, with the pandemic further heightening economic stress and increasing social vulnerability, a major factor driving anti-government sentiment. The major opposition parties have also supported civil society protests in attempts to politically capitalize on the anti-incumbency sentiment prevailing and increasingly manifesting into civil action. FORECAST: Persisting economic deterioration could potentially impact the MPLA’s political consolidation going into municipal elections, which were postponed to 2022.

- In South Africa, similar economic concerns along with a corruption scandal around COVID-19 financial resources also triggered nationwide anti-government protests against the ruling African National Congress (ANC). Major labor union organizations such as Congress of South African Trade Unions (COSATU), which constitute a significant electoral support base for the ANC, have led protests, pressuring the government and the ANC to take action on corruption and other socioeconomic issues. The increasing political pressure to act on the issue indirectly heightened intra-party tensions and factionalism over perceptions of President Cyril Ramaphosa persecuting rival political factions led by former President Jacob Zuma and ANC Secretary General Ace Magashule. FORECAST: The heightened intra-party tensions could undermine the ANC’s political stability, especially ahead of the local elections slated for August 2021.

- FORECAST: Moreover, persisting socioeconomic grievances could potentially trigger increasing anti-incumbency sentiment and weaken the political standing of dominant political forces across the region as seen in Namibia where the South-West Africa People’s Organization (SWAPO) lost considerable ground to the opposition during the municipal elections in November 2020. Furthermore, corruption exposures in the management of COVID-19 finances is another factor that could potentially increase anti-government sentiment, as seen in both South Africa and Malawi. Additionally, an extended economic crisis could also lead to a weakening of other dominant national political forces as well.

Extended pandemic impacts likely to further entrench government authoritarianism in Zimbabwe

- Moreover, extended pandemic impacts are likely to increase concerns related to the government exploiting the health crisis to restrict anti-government activity and crackdown on the population’s rights to free speech and public demonstration. Authorities have already utilized existing emergency and disaster management legislations restrictions to intimidate journalists and activists critical of the government’s management of the pandemic in Angola, Malawi, Mozambique, Zambia, and Zimbabwe.

- In Zimbabwe, the government has utilized the pandemic to further extend its authority and repress the opposition along with any attempts at political protests. Major opposition figures and civil society leaders including journalist Hopewell Chin’ono and Movement for Democratic Change – Alliance (MDC-A) leader Job Sikhala have been arrested with the government effectively suppressing the manifestation of any political dissent. Meanwhile, the government has also resorted to increasing currency and foreign exchange regulation in the economy to counter very steep inflationary trends through 2020.

- FORECAST: Given the situation, the government is likely to continue to utilize social restrictions to repress perceived sources of political dissent and maintain its crackdown against civil society mobilizations, demonstrations, and other such anti-government public events. This could lead to sporadic disruptions to internet and telecommunication services given the government’s disposition to strictly regulate social media and other perceived anti-government media outlets around planned opposition protests.

Increasing socioeconomic stress, vulnerability of low-income populations to manifest into increasing criminal activity

- FORECAST: Most significantly, heightened socioeconomic stress and associated increases in unemployment and poverty carry the potential to lead to an increase in criminal activity. While initial lockdown restrictions witnessed a reduction in crime rates across the region, the trend has reversed over the second half of 2020 and the first quarter of 2021. This is especially a concern in South Africa, Angola, Namibia, and Zimbabwe, who are four out of the top six African countries worst affected by criminality.

- Given the concentration of low income communities in urban localities where crime is heavily entrenched across these countries, increasing criminal activity is particularly likely to affect regional urban localities. FORECAST: The inability of the government to effectively counter these increases is likely to encourage civilian vigilantism, as witnessed in Angola and South Africa. The potential for vigilante justice to spark mob violence could further deteriorate public trust in law enforcement capacity and generally lead to increased insecurity and a potential breakdown in law and order. Such sentiment is likely to further encourage civilian vigilantism, highlighting the risk of cyclical violence between security forces and citizens.

- In Cape Town, South Africa, organized criminal groups and gangs have effectively increased their authority over low income suburban communities capitalizing on the socioeconomic vulnerability of populations there. Criminal activity has also targeted service delivery vehicles, including government relief packages, further entrenching gang dominance over local communities. Similarly, other provinces majorly affected by crime including Gauteng and KwaZulu-Natal have seen an increase in crime over the second half of 2020. FORECAST: Going forward, the situation is likely to translate into an increase in criminal entrenchment across crime focal points in South Africa.

- Additionally, with the countries continuing to face issues in terms of procuring adequate vaccine and medicine supplies, illegal trade in counterfeit vaccines holds the potential to impact national and regional health security. The rush to acquire COVID-19 vaccines across the region could represent a potentially lucrative prospect for organized criminal groups to profit from counterfeit vaccine networks. This was illustrated through the dismantling of a counterfeit vaccine production network with suspected links to China in South Africa in November 2020. FORECAST: While there have been no other reported incidents related to counterfeit vaccines, the potential remains. Meanwhile, illegal trade in counterfeit medicines is likely to continue to pose concerns for national health security.

Recommendations

- Those operating or residing in Southern Africa over the coming weeks and months are advised to practice increased health precautions due to potential exposure to coronavirus and remain cognizant of authorities’ instructions regarding updated quarantines and health procedures.

- Consult with your healthcare provider before traveling. Immediately consult a doctor if you are concerned that you have potentially contracted the disease. Only procedure medication and medical advice from vetted professional institutions and remain cognizant of any fake or counterfeit medication.

- It is advised to remain cognizant of potential disruptions to business continuity over the possibility of increased civil unrest and anti-government protests over the coming months.

- Additionally, it is advised to maintain heightened vigilance over the risk of increasing criminal activity. Foreigners are advised to maintain a low profile due to the heightened crime risk.

Related Reports

-

EconomicsNigeria Analysis: Slow economic growth with high inflation, heightened public frustration to continue in near term in light of President Tinubu’s economic reforms

EconomicsNigeria Analysis: Slow economic growth with high inflation, heightened public frustration to continue in near term in light of President Tinubu’s economic reforms -

PoliticsSouth Africa Analysis: ANC to face significant challenge retaining parliamentary majority in May 29 elections amid internal party struggles, socioeconomic crisis

PoliticsSouth Africa Analysis: ANC to face significant challenge retaining parliamentary majority in May 29 elections amid internal party struggles, socioeconomic crisis -

PoliticsSenegal Analysis: Newly elected President Bassirou Diomaye Faye’s government to face various political, socioeconomic challenges as overall stability persists in near term

PoliticsSenegal Analysis: Newly elected President Bassirou Diomaye Faye’s government to face various political, socioeconomic challenges as overall stability persists in near term -

EconomicsSouth Africa Analysis: Poor economic situation to persist despite some government attempts to stimulate growth, reduce unemployment ahead of May 29 elections

Related Reports

-

EconomicsNigeria Analysis: Slow economic growth with high inflation, heightened public frustration to continue in near term in light of President Tinubu’s economic reforms

-

PoliticsSouth Africa Analysis: ANC to face significant challenge retaining parliamentary majority in May 29 elections amid internal party struggles, socioeconomic crisis

-

PoliticsSenegal Analysis: Newly elected President Bassirou Diomaye Faye’s government to face various political, socioeconomic challenges as overall stability persists in near term

-

EconomicsSouth Africa Analysis: Poor economic situation to persist despite some government attempts to stimulate growth, reduce unemployment ahead of May 29 elections